The world of finance has always been a dynamic one, evolving with the times and adapting to the ever-changing needs of society. The last decade has witnessed one of the most groundbreaking evolutions in the form of cryptocurrencies. These digital currencies, led by the pioneering Bitcoin, have not only introduced a new way of transacting but have also posed unique challenges to the traditional financial system. As with any financial instrument, the need for regulation becomes paramount to ensure stability, trust, and protection for all stakeholders involved. This introduction seeks to provide a comprehensive overview of the current state of cryptocurrency regulations and underscores the significance of these regulations in maintaining financial stability.

The Current State of Cryptocurrency Regulations

- Global Perspective:

- Cryptocurrencies operate on a decentralized platform, meaning they aren’t tied to any specific country or central bank. This global nature has led to a patchwork of regulatory approaches worldwide. While some countries like Japan and Switzerland have embraced cryptocurrencies with open arms and clear regulations, others like China have imposed stringent restrictions or outright bans.

- Regulatory Classifications:

- One of the primary challenges regulators face is how to classify cryptocurrencies. Are they currencies, commodities, securities, or a new asset class altogether? The U.S. Commodity Futures Trading Commission (CFTC) views Bitcoin as a commodity, while the Securities and Exchange Commission (SEC) treats Initial Coin Offerings (ICOs) as securities.

- Consumer Protection:

- With the rise of cryptocurrency exchanges and wallets, ensuring the safety of users’ funds is crucial. Regulations often focus on Know Your Customer (KYC) and Anti-Money Laundering (AML) procedures to prevent fraud and illicit activities.

- Taxation:

- Taxation policies for cryptocurrencies vary widely. In the U.S., the Internal Revenue Service (IRS) treats cryptocurrencies as property, meaning they are subject to capital gains tax. However, this approach isn’t universal, leading to complexities for global traders.

Table 1: Regulatory Approaches in Different Countries

| Country | Classification | Taxation Approach | Notable Regulations |

|---|---|---|---|

| USA | Commodity | Property | SEC oversight on ICOs |

| Japan | Legal Currency | Income Tax | FSA licensed exchanges |

| Switzerland | Asset | Wealth & Income Tax | Crypto-friendly regulations |

| China | Virtual Commodity | Banned | ICOs and exchanges banned |

The Importance of Regulations in Ensuring Financial Stability

- Trust in the System:

- For any financial system to function effectively, trust is paramount. Regulations ensure that cryptocurrency platforms operate transparently and are accountable, fostering trust among users.

- Preventing Financial Crimes:

- Cryptocurrencies, due to their pseudonymous nature, can be misused for illicit activities like money laundering and terror financing. Robust regulations help curb these activities, ensuring the integrity of the financial system.

- Protecting Investors:

- The crypto market is known for its volatility. Regulations help in protecting naive investors from potential scams, Ponzi schemes, and misleading ICOs.

- Economic Stability:

- Unregulated cryptocurrency operations can lead to economic disruptions. For instance, if a widely adopted cryptocurrency crashes, it could have ripple effects on the broader economy. Regulations help in mitigating such systemic risks.

- Encouraging Innovation:

- Contrary to popular belief, regulations aren’t always restrictive. Clear and well-defined regulations can encourage innovation by providing a stable environment for startups and businesses to operate in.

The Rapid Growth and Retreat of the Crypto Ecosystem

The cryptocurrency market, since its inception, has been a rollercoaster of highs and lows, characterized by its rapid growth phases followed by sharp retreats. This dynamic nature, while attracting a plethora of investors looking for high returns, also brings with it a set of challenges and risks that are unique to the crypto ecosystem.

The Volatility of the Crypto Market

- Historical Perspective:

- The crypto market’s volatility is not a new phenomenon. Bitcoin, the pioneer of cryptocurrencies, saw its value skyrocket from mere cents to over $20,000 in 2017, only to drop significantly shortly after. Such price swings have been a recurring theme for many cryptocurrencies, not just Bitcoin.

- Factors Driving Volatility:

- Several factors contribute to the crypto market’s volatility:

- Speculative Nature: Many investors in the crypto market are driven by short-term gains, leading to speculative trading.

- Regulatory News: Announcements related to regulations, such as potential bans or endorsements by governments, can lead to rapid price movements.

- Technological Developments: Innovations, like new blockchain upgrades or the launch of new tokens, can influence market sentiment.

- Market Manipulation: The crypto market, being relatively young, is susceptible to manipulative tactics like “pump and dump” schemes.

- Several factors contribute to the crypto market’s volatility:

- Comparative Volatility:

- When compared to traditional markets, the crypto market’s volatility stands out. While stock markets might consider a 2-3% price movement significant, such fluctuations are commonplace in the crypto world, often occurring within hours.

Challenges and Risks Posed by Market Failures

- Market Failures:

- These refer to situations where the market does not allocate resources efficiently. In the context of the crypto ecosystem, market failures can manifest in various ways, from exchange hacks to misleading Initial Coin Offerings (ICOs).

- Exchange Vulnerabilities:

- Cryptocurrency exchanges, platforms where users buy and sell cryptocurrencies, have been targets for hackers. Notable hacks, like the Mt. Gox incident in 2014, resulted in the loss of millions of dollars worth of Bitcoin, shaking investor confidence.

- Misleading ICOs and Scams:

- The ICO boom around 2017 saw many new projects raising funds by selling their tokens. However, not all were genuine. Some projects disappeared after raising funds, while others failed to deliver on their promises, leading to significant investor losses.

- Lack of Investor Protection:

- Traditional financial markets have mechanisms in place to protect investors, such as insurance on deposits. Such protections are often lacking in the crypto space, making investors vulnerable.

- Systemic Risks:

- The interconnectedness of the crypto ecosystem means that a failure in one part can have ripple effects. For instance, the collapse of a major cryptocurrency or exchange could impact the broader market’s stability.

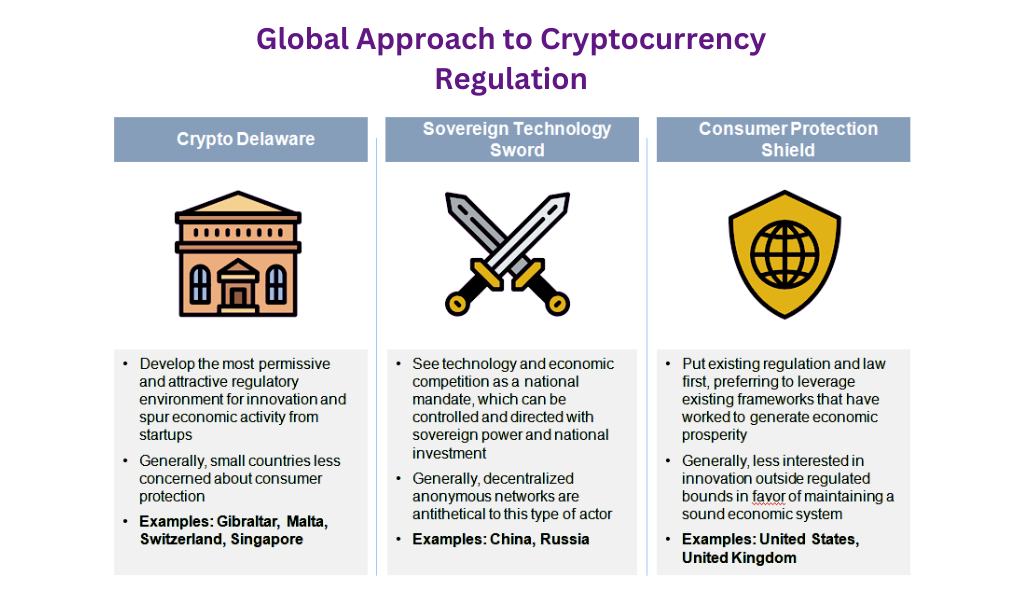

The Global Approach to Cryptocurrency Regulation

Cryptocurrencies, by their very nature, transcend national borders. A decentralized and digital form of currency, they operate on a global scale, making their regulation a complex and multifaceted challenge. As the crypto ecosystem continues to evolve and expand, the need for a coordinated global approach to its regulation becomes increasingly evident. This article delves into the pressing need for global standards and the pivotal role national regulatory authorities play in shaping and implementing these standards.

The Need for Global Standards

- Interconnectedness of the Crypto Market:

- Cryptocurrencies operate on a global network. A Bitcoin transaction, for instance, can be initiated in the U.S. and completed in Japan within minutes. This international nature necessitates a harmonized regulatory approach to ensure consistency and prevent loopholes.

- Avoiding Regulatory Arbitrage:

- In the absence of global standards, there’s a risk of regulatory arbitrage where businesses and traders move operations to countries with lax regulations. This not only undermines stricter regulatory regimes but can also lead to concentration risks.

- Ensuring Investor Protection:

- With investors and traders from various countries participating in the crypto market, global standards can ensure that protective measures are consistent, regardless of where an investor is based.

- Facilitating Innovation:

- Clear and consistent global regulations can provide a stable environment for crypto innovations, ensuring that startups and businesses operate under a unified framework that encourages growth while ensuring safety.

The Role of National Regulatory Authorities

- Implementing Global Standards:

- While global standards provide a blueprint, national regulatory authorities are responsible for adapting and implementing these standards within their jurisdictions. This involves tailoring global guidelines to fit the unique economic, cultural, and legal landscapes of each country.

- Collaboration and Information Sharing:

- National authorities play a crucial role in collaborating with their counterparts in other countries. Sharing information about emerging risks, best practices, and regulatory challenges can foster a more cohesive global approach.

- Enforcement and Oversight:

- It’s one thing to have regulations in place, but their effectiveness hinges on robust enforcement. National authorities are tasked with monitoring crypto activities within their borders, ensuring compliance, and taking corrective actions when necessary.

- Educating the Public:

- Beyond regulation and enforcement, national authorities also play a vital role in educating the public about cryptocurrencies, the associated risks, and the protective measures in place.

- Feedback and Evolution:

- The crypto landscape is ever-evolving. National regulatory authorities, being closer to the ground realities, can provide valuable feedback to global bodies about the effectiveness of existing regulations and areas that need revision or further attention.

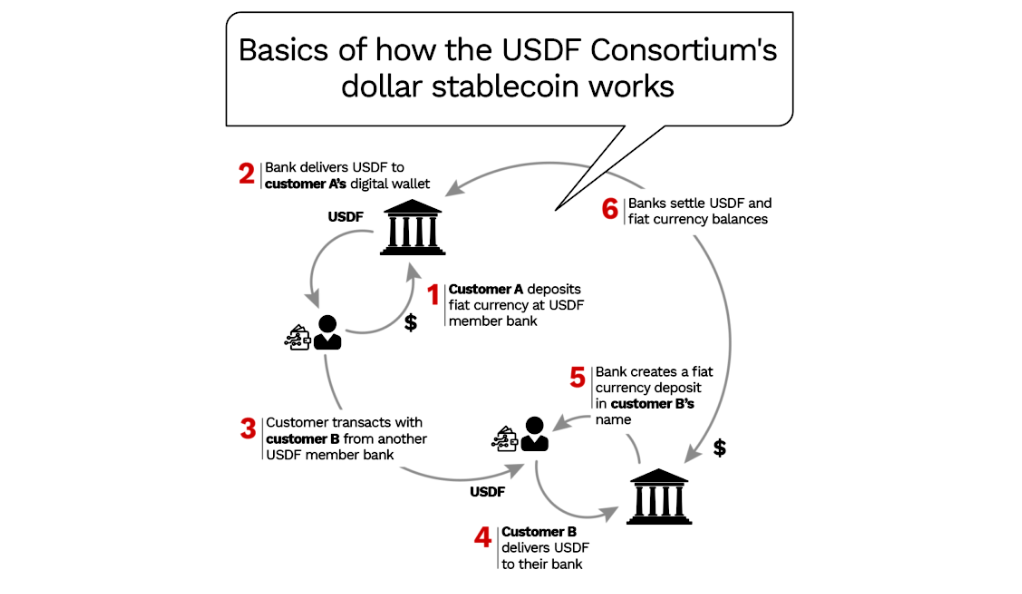

Stablecoins: The New Frontier

In the vast and varied landscape of cryptocurrencies, stablecoins have emerged as a unique and intriguing subset. Designed to bring stability to the notoriously volatile crypto market, stablecoins promise the best of both worlds: the benefits of digital currency combined with the stability of traditional fiat currencies. However, as with any innovation, they come with their own set of challenges and risks. This article delves into the world of stablecoins, exploring their underlying mechanisms and the potential threats they pose to financial stability.

Stablecoins

- What are Stablecoins?

- Stablecoins are a type of cryptocurrency designed to have a stable value, as opposed to the significant volatility seen in cryptocurrencies like Bitcoin or Ethereum. They achieve this stability by being pegged to a reserve or basket of assets, typically traditional fiat currencies like the US Dollar or the Euro.

- Types of Stablecoins:

- Fiat-collateralized: These stablecoins are backed by a reserve of traditional fiat currencies. For every stablecoin issued, there’s an equivalent amount of fiat currency held in reserve. Examples include Tether (USDT) and USD Coin (USDC).

- Crypto-collateralized: These are backed by other cryptocurrencies, like Ether. They maintain stability using mechanisms like liquidation of the collateral should its value drop below a certain threshold.

- Algorithmic: These stablecoins aren’t backed by any collateral. Instead, they use algorithms and smart contracts to automatically increase or decrease the supply of the stablecoin, maintaining its price stability.

Stabilization Mechanisms

- Collateral Management:

- For collateralized stablecoins, issuers maintain reserves equivalent to the number of stablecoins in circulation. Regular audits and transparency reports ensure that the reserves match the circulating supply.

- Over-collateralization:

- Crypto-collateralized stablecoins often hold more than 100% of the stablecoin’s value in cryptocurrency to account for the volatility of the backing crypto assets.

- Liquidation Mechanisms:

- If the value of the collateral drops significantly, portions of it can be automatically sold off to ensure the stablecoin remains fully backed.

- Supply Algorithms:

- Algorithmic stablecoins adjust their supply based on market demand. If the price drops below the peg, the algorithm reduces the supply, and if the price rises above the peg, it increases the supply.

Potential Risks to Financial Stability

- Collateral Vulnerabilities:

- If the value of the collateral, be it fiat or crypto, faces rapid depreciation, it could undermine the stability of the stablecoin.

- Regulatory Scrutiny:

- The backing and issuance of stablecoins, especially fiat-collateralized ones, can attract regulatory attention, leading to potential legal challenges or bans.

- Market Confidence:

- Stablecoins rely heavily on user trust. Any hint of mismanagement or lack of transparency can lead to rapid loss of confidence, causing destabilization.

- Systemic Risks:

- As stablecoins become more integrated with the broader financial system, their failure could have ripple effects, potentially leading to broader financial instability.

- Over-reliance on Algorithms:

- For algorithmic stablecoins, any malfunction or unforeseen loophole in the algorithm could lead to significant price deviations.

Licensing and Authorization of Crypto Asset Service Providers

The meteoric rise of cryptocurrencies and the broader digital asset ecosystem has brought with it a new breed of service providers. These entities, ranging from cryptocurrency exchanges to wallet providers, play a pivotal role in facilitating the adoption and use of digital assets. However, as with any financial service, ensuring the legitimacy, security, and reliability of these providers is paramount. Licensing and authorization emerge as crucial mechanisms in this context. This article delves into the significance of licensing crypto asset service providers, drawing comparisons with traditional financial service providers to highlight the evolving regulatory landscape.

The Importance of Licensing Entities That Provide Core Functions

- Ensuring Trust and Credibility:

- Licensing acts as a stamp of approval, signaling to users that the service provider operates under a set of established guidelines and standards. This fosters trust, a critical component in the financial world.

- Protecting Consumers:

- Licensed entities are often required to implement measures that protect consumers, such as maintaining adequate reserves, implementing robust security protocols, and providing transparent operations.

- Preventing Fraud and Illicit Activities:

- Licensing and oversight can help in identifying and preventing fraudulent activities, ensuring that service providers aren’t complicit in money laundering, terror financing, or other illicit activities.

- Standardizing Operations:

- Licensing provides a framework within which crypto service providers operate, ensuring a level of consistency and standardization across the industry.

Comparing Rules for Traditional Financial Service Providers and Crypto Service Providers

- Regulatory Oversight:

- Traditional Providers: Entities like banks, brokers, and insurance companies operate under stringent regulatory oversight, often governed by central banks or dedicated financial regulatory bodies.

- Crypto Providers: While the regulatory landscape for crypto service providers is still evolving, many jurisdictions are establishing dedicated frameworks or adapting existing financial regulations to oversee their operations.

- Capital Requirements:

- Traditional Providers: They are often required to maintain specific capital reserves to ensure solvency and protect consumers.

- Crypto Providers: Depending on the jurisdiction, crypto service providers might also be subject to capital requirements, especially if they hold customer funds.

- Consumer Protection Mechanisms:

- Traditional Providers: Measures like deposit insurance, dispute resolution mechanisms, and transparency mandates are standard.

- Crypto Providers: While some of these measures are being adopted for crypto entities, the landscape is varied. Some jurisdictions are implementing crypto-specific consumer protection mechanisms, while others are still catching up.

- Anti-Money Laundering (AML) and Know Your Customer (KYC) Protocols:

- Traditional Providers: AML and KYC protocols are well-established, with clear guidelines on customer verification, transaction monitoring, and reporting.

- Crypto Providers: Given the pseudonymous nature of many cryptocurrencies, there’s a heightened focus on implementing robust AML and KYC protocols. However, the decentralized nature of crypto poses unique challenges, leading to varied approaches across jurisdictions.

- Operational Transparency:

- Traditional Providers: Regular audits, financial reporting, and public disclosures are standard practices.

- Crypto Providers: While many leading crypto service providers voluntarily adopt transparency practices, regulatory mandates vary, with some jurisdictions requiring detailed disclosures and others still formulating guidelines.

Addressing the Risks of Multi-Function Entities

In the rapidly evolving world of digital finance, multi-function entities have emerged as versatile players, offering a suite of services under a single umbrella. From exchanges that also provide wallet services to platforms that combine trading, lending, and staking, these entities promise convenience and efficiency. However, their multifaceted nature brings with it a set of inherent risks. This article delves into the complexities of multi-function entities, highlighting the potential dangers they pose and emphasizing the importance of segregating customer assets from other operational functions.

The Dangers of Entities Carrying Out Multiple Functions

- Concentration of Risk:

- Multi-function entities, by virtue of offering multiple services, can become a focal point of risk. A failure in one service area, such as a security breach in the exchange function, can have cascading effects on other services, amplifying the overall impact.

- Operational Complexity:

- Managing diverse functions requires specialized expertise in each area. Entities might struggle to maintain the same level of proficiency across all functions, leading to potential operational inefficiencies or oversights.

- Conflicts of Interest:

- An entity that both manages assets and provides trading services might face situations where its interests don’t align with those of its customers. For instance, using customer deposits for proprietary trading can lead to potential conflicts.

- Regulatory Challenges:

- Different financial services often fall under varied regulatory guidelines. Multi-function entities might find it challenging to comply with multiple sets of regulations simultaneously.

- Liquidity Concerns:

- If customer assets are not segregated, a liquidity crunch in one function, like lending, could impact other services, potentially jeopardizing customer funds.

The Need for Segregating Customer Assets from Other Functions

- Protecting Customer Interests:

- Segregation ensures that customer assets are insulated from any operational risks the entity might face in its other functions. This is crucial for maintaining trust and confidence.

- Ensuring Operational Clarity:

- By keeping assets separate, entities can have a clearer operational framework, with dedicated resources and protocols for each function, leading to more efficient and secure operations.

- Regulatory Compliance:

- Many jurisdictions mandate the segregation of customer assets, especially in the financial sector. Adhering to this not only ensures compliance but also aligns with best practices.

- Enhancing Transparency:

- Segregation allows for clearer accounting and reporting, ensuring that stakeholders have a transparent view of the entity’s operations and financial health.

- Crisis Management:

- In the event of a crisis in one operational area, segregated assets ensure that the impact is contained, preventing a domino effect that could jeopardize the entire entity.

The Role of Central Banks in Regulating Stablecoins

The advent of stablecoins has introduced a novel dimension to the digital currency landscape. Designed to mitigate the volatility typically associated with cryptocurrencies, stablecoins have increasingly come to resemble traditional forms of money. This growing similarity, coupled with the widespread adoption and integration of stablecoins into the financial system, has drawn the attention of central banks worldwide. This article delves into the role of central banks in the context of stablecoins, emphasizing the increasing parallels with traditional money and the consequent need for bank-type regulations.

The Increasing Resemblance of Stablecoins to Traditional Money

- Value Stability:

- Unlike most cryptocurrencies, which can experience significant price fluctuations, stablecoins are designed to maintain a stable value. This is typically achieved by pegging them to traditional fiat currencies, commodities, or other assets.

- Medium of Exchange:

- Due to their stability, stablecoins are increasingly being used as a medium of exchange in digital transactions, much like traditional money. They offer the benefits of digital currencies, such as fast and borderless transactions, without the price volatility.

- Unit of Account:

- As adoption grows, more businesses and platforms are pricing goods and services in stablecoins, further solidifying their role as a standard measure of value.

- Store of Value:

- With their value anchored to stable assets, stablecoins are also being used as a store of value, a function traditionally reserved for fiat currencies and other stable financial instruments.

The Need for Bank-Type Regulation for Stablecoins

- Financial Stability Concerns:

- The widespread adoption of stablecoins could pose risks to financial stability, especially if there are doubts about the value and liquidity of the underlying assets. Central banks, responsible for maintaining financial stability, have a vested interest in ensuring that stablecoins don’t introduce systemic risks.

- Consumer Protection:

- Just as banks are regulated to protect depositors, stablecoin issuers must be held to standards that ensure the safety and accessibility of user funds. This includes mandates on capital reserves, transparency, and operational security.

- Monetary Policy Implications:

- If stablecoins become a significant medium of exchange, they could influence monetary dynamics, potentially affecting central banks’ ability to implement effective monetary policies.

- Preventing Illicit Activities:

- Central banks, in coordination with other regulatory bodies, can ensure that stablecoin operations adhere to stringent Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols, preventing their misuse for illegal activities.

- Ensuring Competitive Neutrality:

- As stablecoins increasingly resemble traditional banking functions, it’s essential to ensure that they are subject to similar regulations, ensuring a level playing field between digital and traditional financial service providers.

Regulating Financial Institutions’ Engagement with Crypto

The integration of cryptocurrencies into the traditional financial system is no longer a distant possibility but a present reality. As financial institutions, from banks to asset managers, increasingly engage with the crypto ecosystem, the need for robust regulatory frameworks becomes paramount. This article delves into the challenges and imperatives of regulating financial institutions’ interactions with cryptocurrencies, emphasizing the importance of clear requirements and addressing the unique risks associated with crypto custody services.

Setting Clear Requirements for Regulated Entities

- Defining the Scope of Engagement:

- Regulatory bodies must delineate the extent to which financial institutions can engage with cryptocurrencies. This could range from allowing direct trading and investment to merely facilitating crypto-related transactions for clients.

- Capital and Liquidity Requirements:

- Given the volatile nature of cryptocurrencies, financial institutions engaging with them might need to maintain higher capital buffers to absorb potential losses. Additionally, liquidity requirements can ensure that institutions can meet their obligations even in volatile market conditions.

- Operational Standards:

- Institutions should adhere to best practices in terms of transaction processing, cybersecurity, and system resilience. Given the unique challenges posed by crypto assets, these standards might differ from those for traditional assets.

- Transparency and Reporting:

- Regulated entities must provide regular disclosures about their crypto-related activities. This includes their exposure levels, the types of crypto assets they hold, and any associated risks.

- Consumer Protection:

- Institutions should clearly communicate the risks associated with crypto investments to their clients. This includes potential price volatility, security concerns, and the evolving regulatory landscape.

Addressing Risks Arising from Custody Services

- Security Concerns:

- Cryptocurrencies, being digital assets, are susceptible to a range of cyber threats, from hacking to phishing. Financial institutions offering crypto custody services must implement state-of-the-art security measures to safeguard these assets.

- Private Key Management:

- The ownership and control of cryptocurrencies hinge on private keys. Institutions must have robust protocols for key management, ensuring that they are securely stored, backed up, and accessible only to authorized personnel.

- Operational Redundancy:

- Given the irreversibility of crypto transactions, custody services should have redundant operational processes to prevent erroneous transfers or losses.

- Insurance and Liability:

- Given the nascent state of the crypto insurance market, institutions must clearly define their liability in the event of losses. Where possible, they should seek insurance coverage for the crypto assets they hold in custody.

- Regulatory Oversight and Audits:

- Regular audits of crypto custody operations can ensure compliance with regulatory standards and identify potential vulnerabilities. External audits, in particular, can provide an added layer of scrutiny and assurance.

Conclusion

The meteoric rise of cryptocurrencies, from niche assets to influential players in the global financial landscape, underscores a pressing reality: the urgent need for comprehensive and forward-thinking regulations. As digital currencies continue to permeate every facet of our financial systems, the absence of robust regulatory frameworks can expose economies to systemic risks, from market volatility to potential misuse for illicit activities.

However, the call for regulation is not merely a reaction to potential threats. It’s a recognition of the transformative potential of cryptocurrencies and the broader blockchain technology. The promise of decentralized finance, borderless transactions, and democratized access to financial services hinges on a stable and trustworthy environment. Regulations, when thoughtfully crafted, can provide this stability.

Yet, the challenge lies in striking a delicate balance. On one hand, there’s a need to manage risks, protect consumers, and ensure the integrity of financial systems. On the other, it’s crucial to foster an environment where innovation can flourish, where startups can experiment without the fear of regulatory backlash, and where the full potential of this revolutionary technology can be realized.

In essence, the urgency for cryptocurrency regulations is not just about managing the present, but about shaping the future. It’s about building bridges between the traditional financial world and the new digital frontier, ensuring that as we step into this future, it’s one marked by security, trust, and boundless innovation.